The September 2022 edition of the Chief Economists Outlook highlighted the intensifying human impact of the cost of living crisis, with plunging real wages leading to worsening poverty and more widespread social unrest.

At the start of 2023, these concerns are still evident, and many households confront a dual challenge of facing relatively high costs for basics such as heating and eating, at the same time as feeling the effects of monetary policy designed to curtail inflation in the longer term.

Related Stories

However, survey respondents indicate that the cost of living crisis may be close to its peak as policies begin to take their full effect, and a majority (68 per cent) expect the crisis to be less severe by the end of 2023

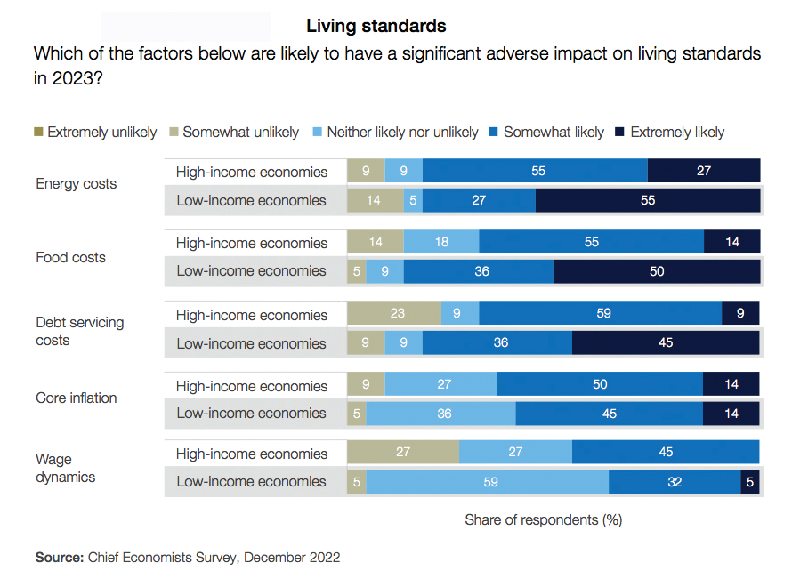

However, the continuing impact of the cost of living crisis should not be underestimated. A majority of respondents are of the view that energy and food costs will continue to have an adverse impact on households in both high- and low-income countries throughout 2023.

Looking at global consumer price inflation data, the food and energy categories recorded the sharpest price increases in 2022, pushed up by a confluence of factors including war, multiple supply chain shocks and commodity market disruption.

Optimism

However, there are some reasons for optimism about food price trends. For example, the Food and Agriculture Organisation (FAO) Food Price Index recently returned to the same level as before the invasion of Ukraine, following the extension of the Black Sea deal that facilitates exports of grain from Ukraine’s ports.

On energy costs, over 80 per cent of respondents expect a significant adverse impact in both developing and developed economies.

On food costs, there is a notable divergence in the expected impact between high- and low-income countries. This is reflected in the much higher proportion of chief economists saying that food costs are extremely likely to have significant adverse impact in low income economies (50 per cent) compared to high-income economies (14 per cent).

Overall, an adverse impact on living standards from food costs is expected by 69 per cent in high income economies and 86 per cent in low-income economies.

This is also evident in the hard data, with low-income countries recording food price inflation of 29 per cent, compared to a global average of 19 per cent.

The World Food Programme now estimates up to 222 million

In addition to rising prices for goods and services, significant increases in borrowing costs are beginning to place an additional strain on household finances.

According to the survey results, there is again a significant divergence between the impact in high-income and low-income economies. In the former, 68 per cent of respondents expect debt servicing costs to have an adverse impact, but only nine per cent say this is extremely likely rather than somewhat likely.

For low income economies, a total of 81 per cent expect an adverse impact, and a much higher proportion (45 per cent ) see this as extremely likely.

On the income side of the cost-of-living squeeze, the respondents expect wage dynamics to have a relatively less adverse impact on households than other cost categories.

Global wages data are patchy and subject to a significant lag, but the latest estimates from the International Labour Organisation (ILO) point to global real wage growth dropping from an average of 1.8 per cent in 2021 to register a year-on-year decline of 0.9 per cent in the first half of 2023.

According to these data, real wages slumped sharply in North America and the EU during this period, falling by 3.2 per cent and 2.4 per cent, respectively, while most other regions recorded slow real wage growth rather than declines.

Relatively, tight labour markets in Europe and North America helped to limit the decline of real wages, while reopening various sectors after lockdowns has led to wage growth, albeit from low levels, in several developing economies.

However, chief economists are split over whether labour markets will remain as tight over the coming year, given the tepid growth prospects, posing a significant potential risk to the expectation of the cost of living crisis ebbing by year-end.

Progress on the energy emergency

Turning to the energy crisis, the majority of respondents (64 per cent) show optimism about the overall trajectory of the crisis in 2023, while also highlighting the need for numerous short-term and long-term policies to deal with challenges that remain to be resolved.

Oil prices have fallen back to prewar levels, but the same is not true of global gas prices, which in November 2022 were 321 per cent higher than two years previously.

The expectation that the energy crisis will be less severe by the end of 2023 reflects the current stress-testing and improvement of systems and processes, diversification of energy supply sources, improved energy efficiency and changing patterns of consumption. Progress in a range of these areas is already evident in Europe, for example, including a tripling of gas reserves, the securing of new supply deals, and a trimming of gas consumption by 15 per cent.

Nevertheless, the crisis remains far from resolved. The survey asked chief economists for their views on the effectiveness of a range of options designed to deal with short-term and long-term challenges posed by the crisis for energy-importing countries. Of the short-term measures, reduction of energy consumption is the preferred one, with 55 per cent of respondents describing it as effective and a further 27 per cent as highly effective.

In addition to easing immediate pressure on the energy system and helping to avoid the worst case scenario of blackouts, reducing energy consumption also minimises the work that needs to be done by other policy responses.

Energy policy to address the crisis

Most of the other policy approaches considered by the chief economists were also viewed as being effective or highly effective by the majority.

However, the use of energy price caps stands out as the most contested option, with an almost equal split between those viewing caps as effective and as ineffective.

This is unsurprising, given the intensity of debate that has surrounded the introduction of a price cap for gas in the EU, including concerns about its potential implications for the financial stability of the Eurozone.

The EU gas price cap, as well as a G7 oil price cap, were approved in December 2022, and it will be some months before there is clear evidence as to their effectiveness.

On long-term energy policies, chief economists were asked to focus on the effectiveness of various measures in terms of achieving energy security for net-importing economies.

Reducing consumption again features prominently, with 86 per cent viewing it as an effective strategy, but is in third place overall.

Improved energy efficiency is the clear front runner, with unanimity among respondents as to its effectiveness in the long term.

This is in line with the International Energy Agency’s (IEA) view that energy efficiency is central to the shift that needs to take place in advanced economies.

Many countries, particularly in Europe, have already begun to move in this direction in response to the crisis. Germany for example, has introduced higher efficiency standards for new buildings, and France launched its “Energy Sobriety” plan in October 2022.

Long-term energy security

Among the other policy options presented, diversification of sources of energy imports were seen as the second most effective option – 90 per cent view it as effective, including 45 per cent as highly effective, the largest proportion for any of the options.

This option will be crucial in Europe, even in the short term. The EU’s ban on oil-product imports from Russia takes effect in February 2023, while reserves of natural gas are projected to be depleted by March 2023.

Although the war in Ukraine is central to the energy crisis in Europe, global security-of-supply concerns in 2023 are unlikely to be driven only by developments in the war. For example, if China’s easing of its zero-COVID restrictions is successful, it is likely to push up demand for liquified natural gas (LNG) and oil products, including diesel, which is becoming increasingly scarce.

Business in the new landscape, Expectations of rough terrain

As the world puts another tumultuous year behind it, chief economists were asked for their views about some of the likely headwinds that businesses in particular are going to face in 2023.

They were also asked about the most effective responses to these headwinds and sources of optimism, which are addressed in the next section.

Among the headwinds, weak demand, higher interest rates and higher input costs stand out. Nine out of ten respondents expect weak demand to exert a significant drag on business activity this year, and almost the same proportion (87 per cent) expect the same of elevated borrowing costs.

Over 60 per cent expect higher input costs to exert a significant drag.

The start of 2023 represents the triple challenge of continued relatively high prices of key inputs meeting tightening monetary policy and weakening demand.

Energy prices are a key factor here, which in turn means that Europe will be particularly exposed, owing to the impact of the war in Ukraine.

According to one recent estimate, the rate of increase of European input costs is set to outpace those of other advanced economies by as much as 20 percentage points from this year, threatening the competitiveness of the region’s producers and running the risk of diverting supply chains and business activity away from the region.

To be Continued…