The Bank of Ghana has disclosed that the eCedi, the Central Bank Digital Currency which it intends to issue will be free of transaction charges to consumers just as in the usage of cash.

Additionally, the banking regulator said in a report released Tuesday that the eCedi was the digital equivalent of the physical cedi by design and as such would not bear interest (i. e. has a zero interest rate), just as cash.

Related Stories

By this approach, the BoG is hopeful that the eCedi would be a strong contender of cash, promote competition in the payment market and facilitate the provision of innovative value-added services to individuals and businesses by banks and payment service providers at affordable fees and charges.

However, the BoG maintains that the eCedi model recognizes and takes into account the value-added service provided by banks, SDIs and payment service providers to facilitate access to and use of eCedi and compensate accordingly.

“In accordance with the liberalization ethos of the Ghanaian financial service industry, BoG does not intend to interfere with the business models of banks, FinTech companies, and merchants regarding fees for eCedi related services,” the report said.

This approach is expected to promote competition in the payment market and facilitate the provision of innovative value-added services on the back of the eCedi ecosystem.

“However, BoG will ensure that the consumers are given fair treatment in every aspect of eCedi transactions by ensuring that banks, SDIs, payment service providers and merchants comply with relevant consumer protection regulations and norms”.

It was not stated in the report whether the proposed Electronic Transfer Levy (E-Levy) will be charged on the payments for value-added services offered by providers.

Read also: ‘Freedom Coin’ investment illegal – BoG to public

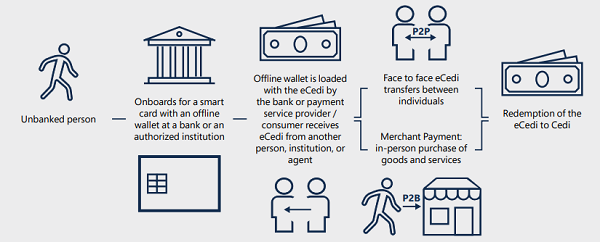

eCedi wallets

According to the report, the BoG has designed two types of wallets for the eCedi:

• Hosted wallets i.e. server-based storage systems that are managed by financial institutions;

• Hardware wallets i.e. secure portable storage devices held by individuals.

The most optimal form factor for the eCedi wallet is the app for a smartphone developed by commercial banks, FinTech companies, and other service providers. Other devices can be utilized depending on user preferences and payment scenarios. These could be smartcards (including the biometric ones) or wearables such as smartwatches that contain communication capabilities and a secure element,” the report states.

Similarly, debit cards and USSD devices (feature phones) which are associated with the existing payment landscape in Ghana can be adapted for eCedi. Thus users can get the type of wallet that suits their needs from a bank or other financial service provider”.

Addressing unregulated/privately issued digital currencies

The Central Bank recently cautioned the general public to exercise caution in respect of cryptocurrency transactions, revealing that no cryptocurrency has the approval to operate in Ghana’s banking and payment sector.

As a result, the central bank is also hopeful that the eCedi will also address risks associated with such unregulated privately issued digital “currencies” or virtual assets.

The scrutiny of Big Tech companies (for instance, Apple, Facebook, or Amazon) in regard to providing payment services and issuing private digital currencies is a significant challenge for regulators nowadays,” the report said.

“Such global private “currencies“, as well as locally issued cryptocurrencies, provoke a wide range of risks including monetary, legal, operational, consumer protection, and financial stability. Digital currency issued and guaranteed by the central bank would meet the demand for digital currencies without posing systemic risks”.

The report also assured that the eCedi balances transparency of transactions with the privacy of consumer data while being fully compliant with the Know Your Customer (KYC) and Anti-Money Laundering/Combating the Financing of Terrorism (AML/CFT) regulations and requirements.